Summary of the key takeaways from Matter and Singapore Fund Directors Association’s recent webinar.

MAS issued guidelines on Environmental Risk Management – Transition Planning (“TPG”) on 5 March 2026, upgrading from the 2020 Environmental Risk Management (ERM) guidelines.

The guidelines supplement the 2020 framework and set out expectations on transition planning for banks, insurers, and asset managers. Our webinar focused on the requirements for asset managers only.

A key point of the guidelines is that they move beyond simple risk identification to forward-looking, strategic transition planning.

TPG applies at entity level (firm's overall strategy) and product level (specific fund metrics), ensuring transparency for clients and regulators

The guidelines will apply from September 2027, following an 18-month transition window starting from the release date (5 March 2026).

While the TPG focus on internal risk management and governance, Singapore’s broader regulatory roadmap for disclosures is explicitly built on the ISSB framework.

MAS has explicitly encouraged financial institutions to reference the ISSB framework and TCFD when finalising transition planning processes.

Think of TPG as the supervisory action and IFRS S2 as the disclosure mechanism:

MAS defines the process of transition planning as the internal risk management processes and strategic planning undertaken by an entity to prepare for climate-related risks and potential changes in business models associated with climate change.

A "transition plan" refers to a documented output of the transition planning process and can be internal documents or externally disclosed.

A credible transition plan for an asset manager is a time-bound strategy that demonstrates how the firm will align its investment activities and business model with a net-zero trajectory, typically targeting 2050 or sooner.

MAS expects asset managers to adapt business models, governance arrangements, and risk management frameworks to address both transition risks (e.g., policy, technology changes) and physical risks (e.g., acute and chronic climate impacts).

Asset managers should engage customers and portfolio companies to understand, and push for progress on, their climate-related risks and management plans, rather than withdrawing investments indiscriminately.

Asset managers should apply risk-materiality-based data collection, meaning data expectations should scale with the materiality of the counterparty’s climate risk profile, avoiding unnecessary burdens.

Asset managers should keep pace with rapid developments in climate-risk methodologies, analytics, and data sources.

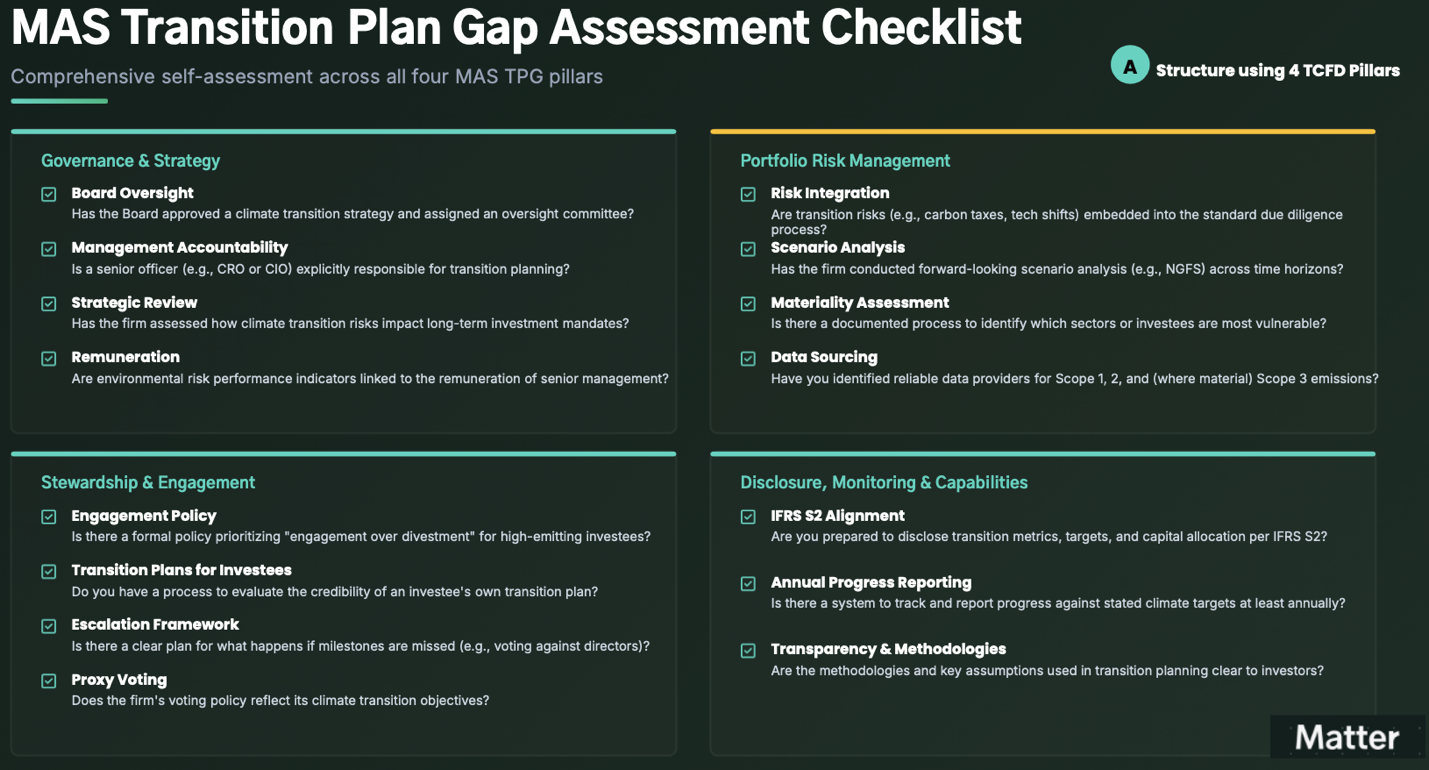

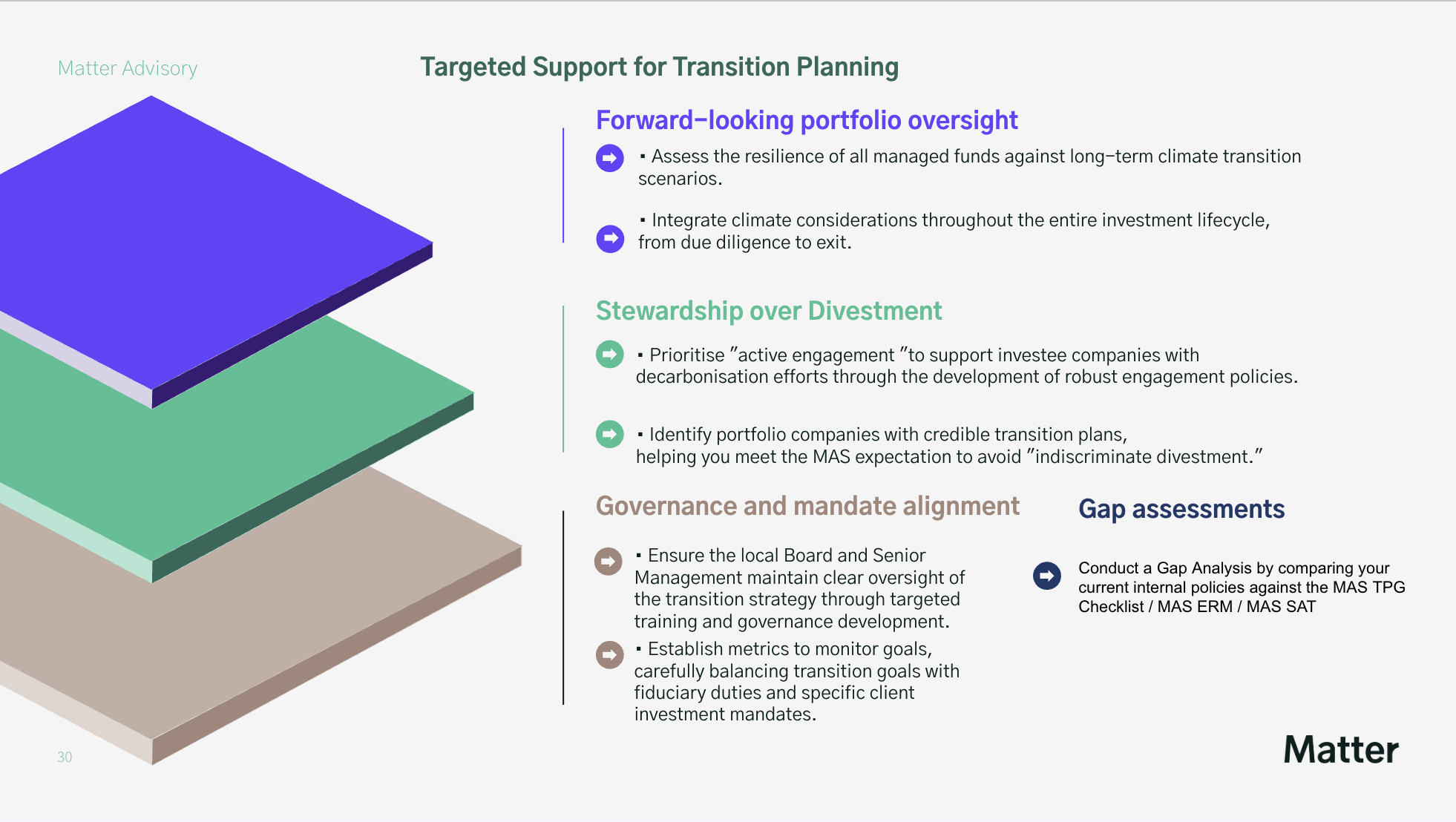

Asset managers could start the process by conducting a gap assessment against the four MAS TPG pillars presented here:

We suggest three key steps in building your transition plan:

A. Structure your report using the 4 Pillars of TCFD.

B. Adopt the specific data requirements of ISSB’s IFRS S2.

C. Refine your sector-specific materiality analysis using the Singapore-Asia Taxonomy (SAT) and SASB metrics.

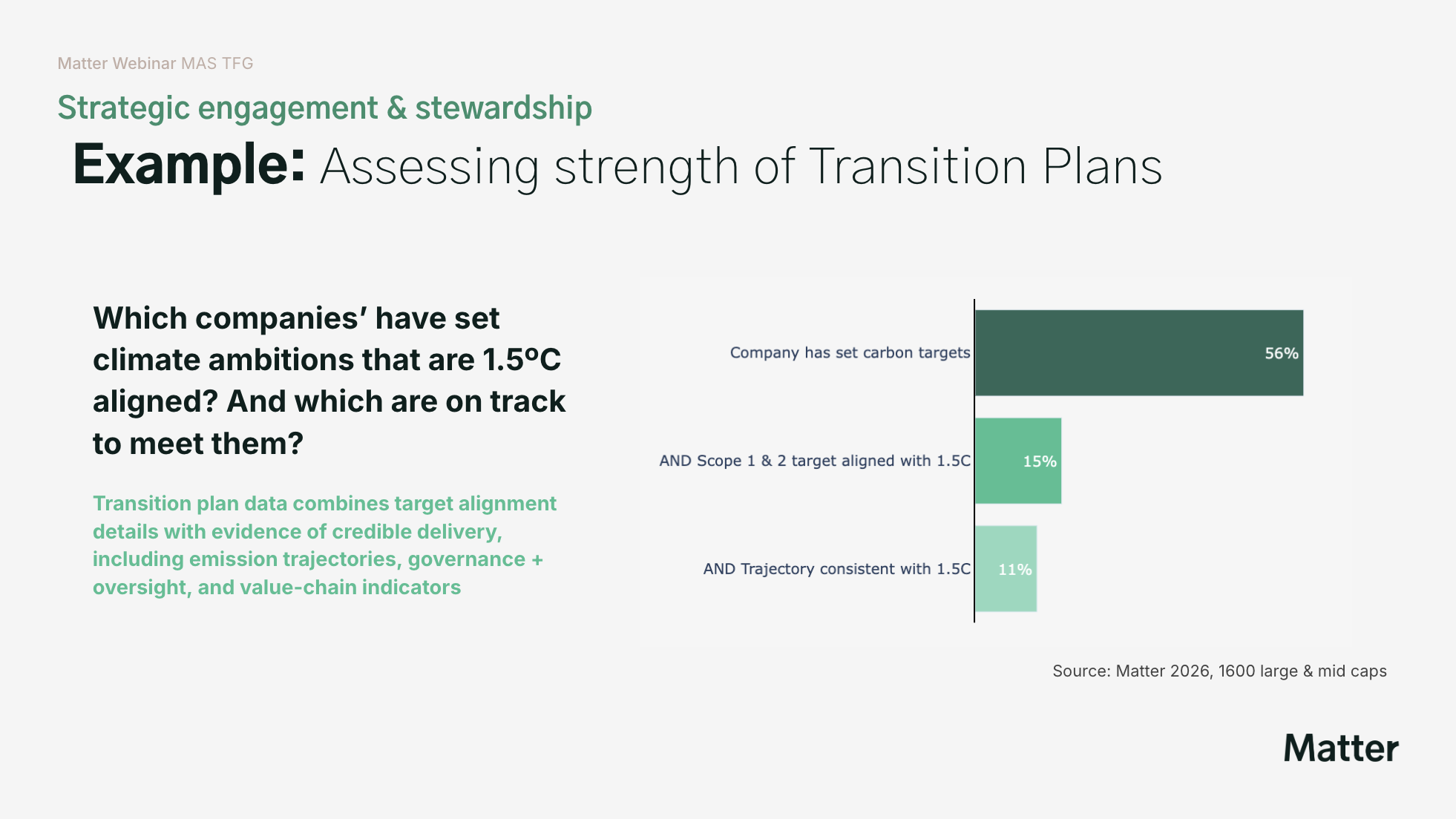

The focus on stewardship is a recognition that asset managers should identify companies - especially in carbon intensive sectors - that have the ability and ambition to transition. Engagement is then used to drive this transition. This also means that data needs to support the idea that companies can viably transition.

Relevant metrics may include:

On the implementation side this allows us to:

Asset managers can think about completing the below steps on your data journey

Matter Advisory can support asset owners and asset managers across the four pillars of the guidelines from Governance and Strategy, Portfolio Risk Management, Engagement, and Disclosure and Monitoring.

Financial institutions must implement structured disclosure practices for GHG emissions associated with their investment portfolios.

Using Matter data, financial institutions can:

Measure GHG emissions disclosures, in line with standardised frameworks

Align with standardised frameworks

Align reporting with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD)

Leverage Forward-Looking Metrics

Support Portfolio Screening & Engagement

Support screening and engagement efforts by identifying companies based on critical transition metrics, including:

You can directly book an introduction call with the team here, share your goals and receive a short gap assessment checklist:

Keep up to date with our webinar, blogs, insights by signing up here: thisismatter.com/insights

MAS issued guidelines on Environmental Risk Management – Transition Planning (“TPG”) on 5 March 2026, upgrading from the 2020 Environmental Risk Management (ERM) guidelines.

The guidelines supplement the 2020 framework and set out expectations on transition planning for banks, insurers, and asset managers. Our webinar focused on the requirements for asset managers only.

A key point of the guidelines is that they move beyond simple risk identification to forward-looking, strategic transition planning.

TPG applies at entity level (firm's overall strategy) and product level (specific fund metrics), ensuring transparency for clients and regulators

The guidelines will apply from September 2027, following an 18-month transition window starting from the release date (5 March 2026).

While the TPG focus on internal risk management and governance, Singapore’s broader regulatory roadmap for disclosures is explicitly built on the ISSB framework.

MAS has explicitly encouraged financial institutions to reference the ISSB framework and TCFD when finalising transition planning processes.

Think of TPG as the supervisory action and IFRS S2 as the disclosure mechanism:

MAS defines the process of transition planning as the internal risk management processes and strategic planning undertaken by an entity to prepare for climate-related risks and potential changes in business models associated with climate change.

A "transition plan" refers to a documented output of the transition planning process and can be internal documents or externally disclosed.

A credible transition plan for an asset manager is a time-bound strategy that demonstrates how the firm will align its investment activities and business model with a net-zero trajectory, typically targeting 2050 or sooner.

MAS expects asset managers to adapt business models, governance arrangements, and risk management frameworks to address both transition risks (e.g., policy, technology changes) and physical risks (e.g., acute and chronic climate impacts).

Asset managers should engage customers and portfolio companies to understand, and push for progress on, their climate-related risks and management plans, rather than withdrawing investments indiscriminately.

Asset managers should apply risk-materiality-based data collection, meaning data expectations should scale with the materiality of the counterparty’s climate risk profile, avoiding unnecessary burdens.

Asset managers should keep pace with rapid developments in climate-risk methodologies, analytics, and data sources.

Asset managers could start the process by conducting a gap assessment against the four MAS TPG pillars presented here:

We suggest three key steps in building your transition plan:

A. Structure your report using the 4 Pillars of TCFD.

B. Adopt the specific data requirements of ISSB’s IFRS S2.

C. Refine your sector-specific materiality analysis using the Singapore-Asia Taxonomy (SAT) and SASB metrics.

The focus on stewardship is a recognition that asset managers should identify companies - especially in carbon intensive sectors - that have the ability and ambition to transition. Engagement is then used to drive this transition. This also means that data needs to support the idea that companies can viably transition.

Relevant metrics may include:

On the implementation side this allows us to:

Asset managers can think about completing the below steps on your data journey

Matter Advisory can support asset owners and asset managers across the four pillars of the guidelines from Governance and Strategy, Portfolio Risk Management, Engagement, and Disclosure and Monitoring.

Financial institutions must implement structured disclosure practices for GHG emissions associated with their investment portfolios.

Using Matter data, financial institutions can:

Measure GHG emissions disclosures, in line with standardised frameworks

Align with standardised frameworks

Align reporting with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD)

Leverage Forward-Looking Metrics

Support Portfolio Screening & Engagement

Support screening and engagement efforts by identifying companies based on critical transition metrics, including:

You can directly book an introduction call with the team here, share your goals and receive a short gap assessment checklist:

Keep up to date with our webinar, blogs, insights by signing up here: thisismatter.com/insights